Table of Contents

Delivery Duty Unpaid: Incoterm Mistakes Procurement Makes

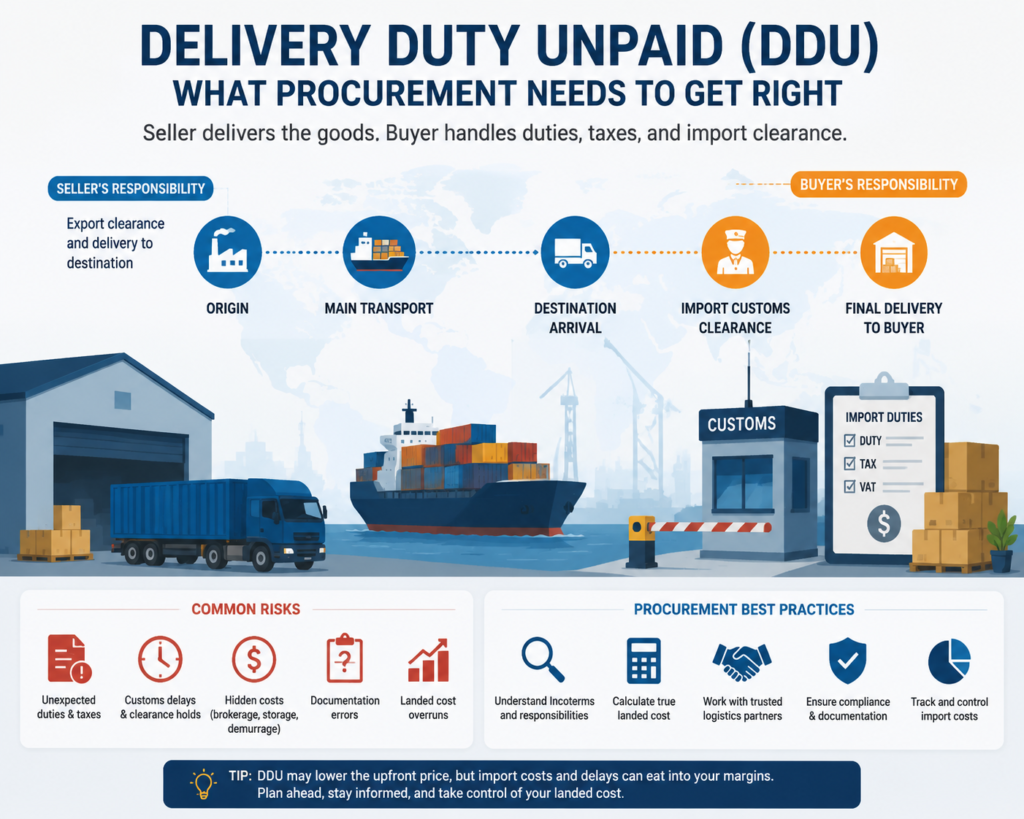

In global procurement reality, Delivery Duty Unpaid (DDU) continues to surface in contracts, RFQs, and supplier negotiations, often creating cost leakage points that only appear after shipment arrival. Understanding its structure is critical for purchase engineers managing cross-border sourcing at scale.

1. Delivery Duty Unpaid in Global Procurement Strategy

Definition of DDU in cross-border trade

Delivery Duty Unpaid sits in a transitional logistics structure where the seller delivers goods to a destination but excludes import duties, VAT, and customs clearance responsibilities. In procurement execution, this creates a split responsibility model where export logistics are handled upstream, but import obligations are pushed downstream to the buyer. It often leads to hidden cost accumulation once goods reach destination customs. For technical buyers, this structure behaves like an “incomplete landed cost package” that only reveals its full expense at the border stage.

How DDU shifts responsibility between buyer and seller

Under this structure, sellers manage export clearance and main carriage, while buyers absorb customs entry, tax payments, and regulatory compliance at destination. This division creates operational ambiguity when shipments encounter customs inspection or documentation issues. In practice, responsibility shifts mid-stream, making it harder to assign accountability when delays occur. Many procurement teams underestimate how heavy the destination-side workload becomes until shipments are physically stuck at port.

Why procurement teams still encounter DDU in sourcing contracts

Despite modern Incoterms updates, DDU still appears in legacy agreements and supplier-driven templates. It persists because suppliers prefer minimizing unpredictable import exposure, while buyers sometimes accept lower upfront pricing without fully analyzing downstream obligations. In fragmented global supply chains, especially cross-border sourcing in Asia-Europe and Asia-Americas lanes, DDU continues to survive as a default fallback structure. It often shows up unexpectedly in contracts where procurement governance is not strictly standardized.

2. How Delivery Duty Unpaid Impacts Total Landed Cost

Separation of product cost and import charges

DDU pricing separates product cost from import-related expenses, creating an illusion of cost clarity at the purchase order stage. However, this separation removes visibility over the true landed cost structure. Import charges such as duties and handling fees remain outside the supplier invoice, creating downstream financial exposure. Procurement teams often realize too late that the “real cost” begins after shipment arrival.

Hidden customs and tax exposure for buyers

Once goods arrive, customs duties, VAT, brokerage fees, and inspection charges become the buyer’s responsibility. These costs vary significantly by country and product classification, making them difficult to forecast accurately. A minor HS code deviation can trigger entirely different tariff treatment. This creates a scenario where cost surprises hit the procurement budget like an unplanned surcharge wave.

Misalignment between PO price and final cost

The purchase order may reflect an optimized unit price, but the final landed cost often tells a different story. This misalignment disrupts cost forecasting and internal financial reporting. Procurement, finance, and operations teams frequently struggle to reconcile these discrepancies. In real sourcing environments, the invoice price is only the starting point, not the full economic reality.

3. Key Responsibilities Under Delivery Duty Unpaid

Seller obligations before export shipment

The seller is responsible for export packaging, export clearance, and delivering goods to the destination port or agreed point. This includes ensuring export compliance and arranging international transport. However, the seller is not responsible for import clearance or destination-side taxes. This creates a clear but limited scope of responsibility on the supplier side.

Buyer obligations at destination customs

Buyers must handle import declarations, customs duties, VAT, and coordination with local customs brokers. This often requires regulatory knowledge and operational readiness in the destination country. Without proper infrastructure, shipments can remain stuck at customs facilities. Procurement teams often find themselves acting as unplanned import operators.

Risk ownership during transit and clearance

Risk allocation under DDU is complex because physical transport and financial responsibility do not always align. While transport may be handled by the seller, financial exposure during customs delays is often absorbed by the buyer. This creates ambiguity when delays, inspections, or regulatory interventions occur. In practice, this is where most disputes in cross-border logistics arise.

4. Why Procurement Professionals Misunderstand DDU Terms

Confusion with DDP and other Incoterms

DDU is frequently confused with DDP, DAP, and other trade terms, leading to misinterpretation of cost responsibility. Many procurement professionals assume “delivered” means fully inclusive pricing, which is incorrect under DDU. This misunderstanding often leads to budget miscalculations. Incoterms clarity is essential to avoid structural cost errors.

Lack of visibility into destination regulations

Customs regulations vary widely across jurisdictions, affecting duties, documentation, and compliance requirements. Without local regulatory insight, procurement teams cannot accurately forecast import costs. Even small regulatory updates can significantly impact landed cost structures. This lack of visibility introduces unavoidable uncertainty.

Over-reliance on supplier shipping terms

Procurement teams often accept supplier-defined shipping terms without independent validation. This creates dependency on external interpretations of logistics responsibility. Suppliers may prioritize simplicity over buyer-side cost optimization. As a result, procurement decisions are made with incomplete operational data.

5. Common Contract Mistakes in DDU Agreements

Missing clarification of customs duties

Contracts often fail to clearly define responsibility for customs duties and taxes. This leads to disputes when shipments arrive and unexpected charges appear. Clear contractual allocation is essential for financial predictability. Without it, ambiguity becomes a recurring cost risk.

Vague delivery point definitions

Unclear delivery definitions create confusion over where responsibility transfers. Whether delivery is at port, warehouse, or facility must be explicitly defined. Otherwise, additional handling and logistics charges may emerge. Precision in delivery terms is critical in procurement contracts.

Lack of agreed clearance responsibilities

Many agreements do not specify who manages customs clearance processes in detail. This leads to operational delays when goods arrive. Both parties may assume the other is responsible. This gap creates avoidable friction at destination ports.

6. Customs Clearance Risks in DDU Shipments

Unexpected delays at port of entry

Ports are high-pressure environments where minor issues can escalate into major delays. Under DDU, buyers face these delays without upstream support. Even routine inspections can extend clearance timelines significantly. This disrupts downstream production schedules.

Documentation errors causing holds

Incorrect invoices or missing HS codes can trigger customs holds immediately. These issues are common in international shipments. Once flagged, corrections require time and additional cost. Documentation accuracy is essential for smooth clearance.

Import compliance gaps for brand goods

Certain branded or regulated goods require strict compliance documentation. Under DDU, buyers are responsible for securing these approvals. Missing compliance steps can result in shipment rejection. This creates significant operational risk for procurement teams.

7. Hidden Cost Drivers in Delivery Duty Unpaid Models

Duties, VAT, and local taxes variations

Tax structures vary widely across countries, making cost prediction difficult. Even similar products may face different tariff classifications. This creates volatility in procurement budgeting. Cost control becomes challenging under such variability.

Brokerage and handling fees at destination

Customs brokers and terminal operators charge additional fees during clearance. These costs are often underestimated in procurement planning. Multiple small charges accumulate into significant totals. This creates hidden financial pressure.

Storage and demurrage penalties

Delays in clearance trigger storage and demurrage fees at ports. These charges escalate quickly over time. Procurement teams often discover them only after shipment release. They represent one of the most avoidable cost risks.

8. Supply Chain Visibility Challenges Under DDU

Limited tracking of customs status

Once shipments enter customs, visibility often decreases significantly. Tracking systems rarely provide real-time clearance updates. This creates uncertainty in logistics planning. Procurement teams are forced into reactive decision-making.

Lack of cost transparency before arrival

Import costs remain unknown until goods reach destination customs. This delays financial planning and reconciliation. Procurement loses the ability to fully forecast landed cost. This reduces budgeting accuracy.

Difficulty forecasting landed cost accurately

Without stable duty structures, landed cost modeling becomes unreliable. Variations in tariffs and clearance fees distort projections. This impacts procurement strategy and supplier evaluation. Forecast accuracy becomes a major challenge.

9. Impact of DDU on Brand Procurement Budgets

Budget variance from unexpected import charges

Unexpected customs charges frequently disrupt procurement budgets. These variances often appear after shipment arrival. Finance teams must adjust allocations reactively. This reduces financial predictability.

Reduced margin control in sourcing decisions

Unpredictable import costs reduce control over final product margins. Procurement decisions may become less accurate. Profitability can be impacted across product lines. Margin erosion becomes a hidden risk.

Difficulty standardizing global procurement costs

Different countries create different import cost structures. This prevents standardization of global procurement budgets. Each shipment behaves differently financially. Consistency becomes difficult to achieve.

10. Supplier Negotiation Risks in DDU Transactions

Suppliers shifting cost burden to buyers

DDU allows suppliers to transfer import responsibility to buyers. This reduces supplier risk exposure. However, it increases buyer-side cost complexity. Negotiation balance becomes critical.

Weak leverage in contract negotiation

Buyers without alternative terms often lose negotiation leverage. Suppliers can dictate shipping structures. This weakens procurement influence. Strategic negotiation is required.

Inconsistent Incoterm interpretation

Different suppliers interpret DDU differently in practice. This creates inconsistencies across shipments. Procurement teams face operational confusion. Standardization becomes difficult.

11. How DDU Affects Lead Time and Delivery Reliability

Customs delays affecting production schedules

Customs delays can disrupt production timelines significantly. Manufacturing schedules depend on timely delivery. Any delay cascades through operations. This impacts overall efficiency.

Unpredictable clearance timelines

Clearance times vary based on documentation and inspections. Under DDU, buyers absorb this unpredictability. Planning becomes difficult. Time buffers are often required.

Impact on inventory planning and stockouts

Uncertain delivery timing affects inventory planning. Stockouts or overstock situations may occur. This increases operational inefficiency. Supply chain stability is affected.

12. Difference Between DDU, DDP, and DAP for Procurement

Responsibility comparison across Incoterms

DDU places import responsibility on buyers, DDP places it on sellers, and DAP splits responsibilities differently. Each structure changes risk allocation. Procurement teams must understand these differences clearly. Misinterpretation leads to cost issues.

Cost structure differences for buyers

DDP offers predictable pricing, while DDU introduces variable import costs. DAP sits in between depending on arrangement. Cost visibility differs significantly. Procurement must evaluate accordingly.

Risk allocation variations in real operations

Operational reality often differs from theoretical Incoterms definitions. Customs delays and compliance issues shift risk dynamically. Procurement must account for this gap. Real-world execution matters more than definitions.

13. Documentation Requirements Under DDU Shipping

Commercial invoice accuracy requirements

Accurate invoices are essential for customs clearance. Errors can trigger inspections or delays. Procurement teams must validate documentation carefully. Precision reduces risk.

Packing list and HS code importance

Packing lists and HS codes determine classification and duty rates. Misclassification increases cost and risk. These documents are critical for compliance. Accuracy ensures smoother clearance.

Import permits and compliance paperwork

Certain goods require import permits and certifications. Buyers must manage these requirements under DDU. Missing paperwork can block shipments. Compliance readiness is essential.

14. Risk Management Strategies for Procurement Teams

Building contingency into landed cost models

Procurement teams should include buffer costs in landed cost calculations. This accounts for variability in duties and fees. Without buffers, budgets become unstable. Risk planning is essential.

Supplier qualification based on logistics capability

Evaluating supplier logistics capability reduces operational risk. Experienced suppliers handle documentation better. This improves reliability. Capability matters beyond price.

Insurance coverage considerations

Cargo insurance mitigates transit risk but not customs delays. Procurement must understand coverage limits. Insurance supports but does not eliminate risk. It is part of a broader strategy.

15. How to Evaluate Suppliers Using DDU Terms

Assessing export experience and capability

Experienced exporters manage documentation more effectively. This reduces clearance risk. Procurement should assess supplier history. Experience improves reliability.

Reviewing historical customs performance

Past performance indicates future reliability. Frequent delays signal weak processes. Data-driven evaluation is essential. History provides insight.

Measuring transparency in cost breakdowns

Transparent suppliers provide clear cost structures. This improves landed cost accuracy. Lack of transparency increases uncertainty. Visibility is essential for procurement control.

16. Industry Scenarios Where DDU Commonly Appears

Cross-border e-commerce sourcing models

E-commerce shipments often use DDU for simplicity. Buyers handle import duties locally. This reduces supplier complexity. It is widely used in small parcel logistics.

Small and mid-sized supplier shipments

SMEs frequently use DDU due to limited logistics infrastructure. This shifts complexity to buyers. Procurement teams must manage import processes. It is a common structure.

Trial orders and sample procurement flows

Sample shipments often use DDU to reduce supplier burden. Buyers handle import clearance for evaluation orders. This simplifies initial transactions. It is common in sourcing cycles.

17. How to Convert DDU Agreements into Controlled Procurement Models

Negotiating shift toward DAP or DDP terms

Procurement teams can negotiate more controlled Incoterms. DAP or DDP improves cost predictability. This reduces import uncertainty. Negotiation strength is key.

Structuring hybrid logistics agreements

Hybrid models balance cost control and flexibility. Responsibilities are shared strategically. This improves operational efficiency. It is suitable for mature supply chains.

Standardizing Incoterm clauses in contracts

Standard clauses reduce ambiguity in agreements. This improves consistency across suppliers. Procurement governance becomes stronger. Standardization reduces risk.

18. Best Practices for Procurement Cost Control Under DDU

Building landed cost calculation frameworks

Structured models help forecast total import costs. These include duties, taxes, and fees. This improves budgeting accuracy. Data-driven planning is essential.

Using logistics partners for clearance visibility

Logistics partners provide customs visibility and support. This reduces uncertainty in clearance timelines. Procurement gains operational insight. Visibility improves control.

Implementing centralized import cost tracking systems

Centralized systems consolidate all import expenses. This improves reporting and cost control. Procurement efficiency increases over time. Centralization strengthens governance.

Reference resources: Incoterms Overview | ICC Incoterms Rules | WTO Customs Valuation | U.S. Customs and Border Protection