Table of Contents

1. Introduction to China to Europe Import VAT

What import VAT means in cross-border trade

Import VAT in cross-border trade functions as a fiscal gatekeeper imposed at the point of entry into the European market, essentially acting like a consumption tax prepayment that ensures goods originating from outside the EU are brought into parity with domestically circulated products. From a purchase engineering standpoint, it is not merely a tax line item but a structural cost variable that directly reshapes landed cost architecture, especially when shipments scale from sporadic sourcing to continuous supply chain pipelines where every percentage point quietly compounds into budget distortion.

Why EU VAT rules matter for Chinese imports

EU VAT rules are not just bureaucratic formalities; they are a regulatory lattice that dictates how value is recognized, declared, and ultimately taxed when goods arrive from China, and overlooking them is like building procurement strategy on shifting sand. In real-world sourcing scenarios, inconsistent VAT treatment across EU member states can trigger unexpected cash outflows, delayed clearance, or even cargo immobilization.

Impact on global procurement strategies

From a strategic procurement lens, import VAT reshapes sourcing calculus by influencing supplier selection, Incoterms negotiation, and even inventory positioning decisions, because VAT exposure can either be deferred, reclaimed, or locked as sunk cost depending on structuring finesse.

2. Overview of EU Import VAT System

Structure of VAT in the European Union

The EU VAT system operates as a harmonized yet locally administered framework, meaning each member state applies its own rate while adhering to overarching EU directives.

Differences between VAT and customs duty

VAT and customs duty are often confused, but they serve fundamentally different fiscal purposes: customs duty is a trade policy instrument, while VAT is a consumption-based tax.

Key VAT principles for imported goods

Imported goods are taxed based on destination principle taxation, ensuring a level playing field between EU-produced and imported goods.

Reference: Value Added Tax Overview

3. How Import VAT is Calculated in the EU

Taxable value components

The taxable base for import VAT typically includes the customs value of goods plus applicable duties.

Inclusion of freight and insurance costs

Freight and insurance are usually embedded into the taxable value, meaning logistics decisions directly influence tax exposure.

Country-specific VAT rate differences

Although the EU shares a common VAT framework, rates vary significantly across member states.

4. Customs Clearance Process in the EU

Step-by-step import clearance flow

The clearance process begins with pre-arrival data submission, followed by valuation review, VAT calculation, inspection, and release authorization.

Role of customs authorities in VAT collection

Customs authorities act as fiscal intermediaries for VAT collection at the border.

Required documentation during clearance

Essential documents include commercial invoices, packing lists, bill of lading, and customs declarations.

Reference: European Commission VAT System

5. Key VAT Registration Requirements

When foreign sellers need VAT registration

Foreign suppliers may need VAT registration when storing goods in the EU or selling directly to consumers.

Role of EU VAT numbers for importers

An EU VAT number enables businesses to reclaim input VAT and operate within the tax system transparently.

Impact of EORI registration

The EORI number functions as a customs identity key required for import clearance.

6. Importer of Record Responsibilities

Definition of importer of record (IOR)

The importer of record is the legal entity responsible for ensuring goods comply with import regulations and taxes are properly paid.

VAT liabilities for procurement teams

When acting as IOR, procurement teams assume direct VAT liability.

Risk allocation in supply chains

Risk allocation depends heavily on contractual structuring and Incoterms selection.

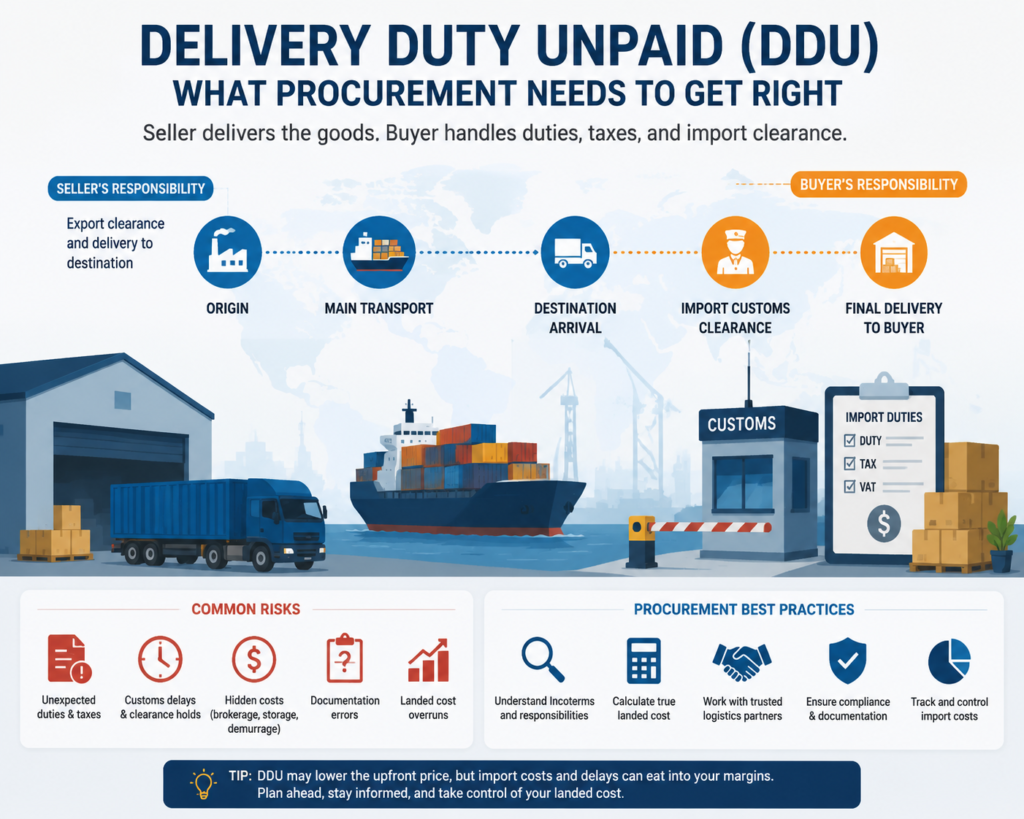

7. DDP vs DAP in EU Imports

Differences in VAT handling under DDP

Under DDP terms, the seller assumes responsibility for VAT and customs clearance.

Cost implications for procurement buyers

DAP shifts VAT responsibility to the buyer, requiring upfront cash flow allocation.

Risk control in each shipping term

DDP reduces operational risk but increases supplier dependency.

8. VAT Payment Timing and Cash Flow Impact

When VAT is paid during import process

VAT is typically paid at customs clearance, creating upfront cash flow pressure.

Deferred VAT accounting options

Certain EU countries allow deferred VAT accounting to improve liquidity.

Cash flow planning for importers

Effective planning synchronizes procurement cycles with tax obligations.

9. VAT Deduction and Recovery Mechanisms

Input VAT recovery eligibility

Input VAT can generally be recovered if goods are used for taxable business activities.

Documentation needed for VAT reclaim

Reclaiming VAT requires invoices, import declarations, and proof of payment.

Common mistakes in VAT recovery

Frequent errors include mismatched invoices and incorrect VAT numbers.

10. Country-Level VAT Differences in Europe

VAT variations across major EU markets

Different EU countries apply varying VAT rates affecting landed cost.

Impact on multi-country distribution

Multi-country distribution increases compliance complexity significantly.

Strategic planning for regional imports

Strategic planning involves selecting optimal entry points for tax efficiency.

11. Customs Valuation Rules in the EU

Methods used to determine customs value

Customs value is determined using transaction value methods.

Treatment of transfer pricing and invoices

Transfer pricing must align with customs valuation rules.

Adjustments affecting VAT base

Royalties and tooling costs may be included in customs value.

Reference: World Customs Organization

12. Common VAT Compliance Risks

Misclassification of goods

Incorrect HS classification leads to incorrect VAT and duty application.

Undervaluation issues

Undervaluing goods can result in penalties and audits.

Documentation errors in customs declarations

Even minor inconsistencies can trigger compliance reviews.

13. Impact of Import VAT on Total Landed Cost

VAT as part of total landed cost structure

VAT significantly contributes to landed cost and impacts pricing models.

Pricing strategy implications for procurement

Procurement pricing must incorporate VAT exposure to avoid margin erosion.

Margin pressure on imported goods

VAT can compress margins if not properly reclaimed.

14. VAT Optimization Strategies for Importers

Structuring supply chains efficiently

Efficient structuring reduces overall tax friction.

Use of fiscal representatives in the EU

Fiscal representatives manage VAT obligations on behalf of foreign entities.

Leveraging bonded warehousing

Bonded warehouses allow VAT deferral until goods enter circulation.

15. Role of Freight Forwarders in VAT Management

Support in customs documentation

Freight forwarders assist in preparing accurate documentation.

Coordination with EU customs brokers

They act as intermediaries between importers and customs brokers.

Reducing compliance risks in logistics

They minimize risk of delays and penalties through procedural accuracy.

16. Digital Customs Systems in the EU

Introduction to EU import digitalization

The EU is progressively digitizing customs processes through electronic declarations.

Automated VAT processing systems

Automation reduces human error and improves tax calculation accuracy.

Benefits for cross-border procurement

Digital systems improve clearance speed and predictability.

17. Brexit and Its Impact on Import VAT

VAT changes for UK vs EU imports

Brexit introduced a clear VAT separation between UK and EU systems.

Dual compliance requirements

Companies must maintain separate VAT registrations.

Adjustments in logistics routing

Supply chains have been rerouted for tax efficiency.

18. Industry-Specific VAT Considerations

Electronics and high-value goods

High-value goods require precise valuation and documentation control.

Apparel and fast-moving consumer goods

High turnover products require efficient VAT recovery cycles.

Industrial equipment and machinery imports

Complex valuation arises due to installation and service components.

19. Case Study: China to Europe Import Flow

Typical VAT cost breakdown example

A standard import includes product cost, freight, duty, and VAT.

Common operational challenges

Challenges include documentation mismatches and clearance delays.

Optimization outcomes for importers

Optimized flows improve margin predictability and clearance speed.

20. Future Trends in EU Import VAT Regulations

Expected regulatory tightening

The EU is moving toward stricter enforcement and transparency.

Digital tax reporting expansion

Real-time reporting systems will increase data requirements.

Implications for global procurement teams

Procurement teams must integrate tax intelligence into sourcing decisions.